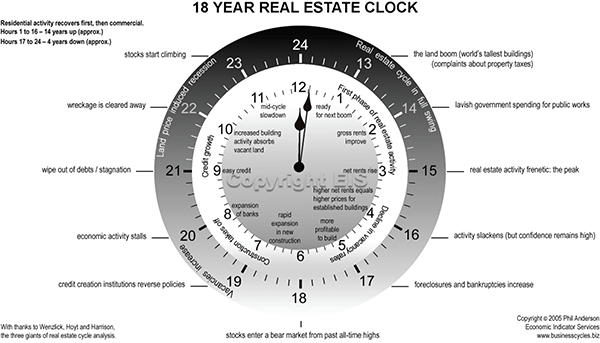

The property clock is a simple way for investors to understand where the market sits in the real estate market cycle. It shows how property

Co-living properties for sale are attracting more attention as Australia continues to face strong housing demand, rising rental costs and limited supply in many areas.

Tired of searching for affordable housing? Ever wished you could live in a cool, renovated space with a built-in community? Well, there’s a trend taking

The Australian property market has always moved in cycles, but investors who focus only on timing often overlook the power of strategy. While growth phases,